Stay in the loop

Sign up for event alerts, as well as insights from our experts.

Seventy-seven percent of global online purchases are made with what many still label ‘alternative payment methods’ rather than with a credit card.

If you don’t offer the right local payment methods for the countries you sell in, your customers will bounce before they buy. Integrating these local payment methods can be costly and time-consuming – if you try to do it all yourself. Whether you plan to open a local online marketplace or sell cross-border, you must offer a locally preferred frictionless payment method.

What you’ll learn & what is covered

There are eleven common types of local digital payment methods. Here’s a list:

Bank-transfer apps take funds from the customer’s bank account and send them to the merchant. Usually, these are push payments. In their online or mobile banking app, the customer checks the amount and authorises the payment. Transfers may take several business days. But thanks to real-time interbank payment systems, funds are often transferred within seconds.

PPRO offers multiple bank transfer methods, such as BLIK, iDEAL and Trustly.

Buy Now Pay Later payment methods let customers do exactly what the name suggests, buy something now but pay at a later date. Many allow customers to pay thirty days after the purchase date. Some also allow the customer to pay in installments or even with post-dated payments. Some BNPL payment methods are online only, some can also be used in stores.

PPRO offers multiple BNPL payment methods, such as Afterpay, and Zip.

The most well-known cards are Visa and Mastercard. But there are also lots of local card schemes, specific to a country or region. These alternative payment cards can be co-badged with international card brands for wider acceptance. Some prominent examples are RuPay in India and Troy in Turkey.

Virtual cards

Virtual cards allow customers to pay online without entering or revealing their bank or card details. The cards are usually single-use or available for a limited time only.

Card wallets

Card wallets are mobile apps that link to the customer’s store-payment card. A secure, tokenised card number is generated for each transaction. This is a secure and convenient way for customers to shop online, and sometimes in-app or in-store, without having to enter or reveal card details.

E-wallets

Like a real wallet, an e-wallet is a way to store money. Customers load cash onto their e-wallet using a bank-transfer, their credit card or even by paying cash at a participating store. They can then use their e-wallet to shop, either online or in store. Customers need internet access via a desktop, laptop or mobile device to use an e-wallet. Popular examples include Alipay, WeChat Pay, PayPal and Skrill.

Mobile wallets

Customers must have a mobile phone to use a mobile wallet — but not always a smartphone. This is the difference between a mobile wallet and an e-wallet. Customers load their mobile wallets by paying cash at a participating store, using carrier billing or with a bank transfer. They can then use them to pay online and perform other transactions. Some mobile wallets link directly to the customer’s bank account, others don’t need the customer to even have a bank account.

Pass-through wallet

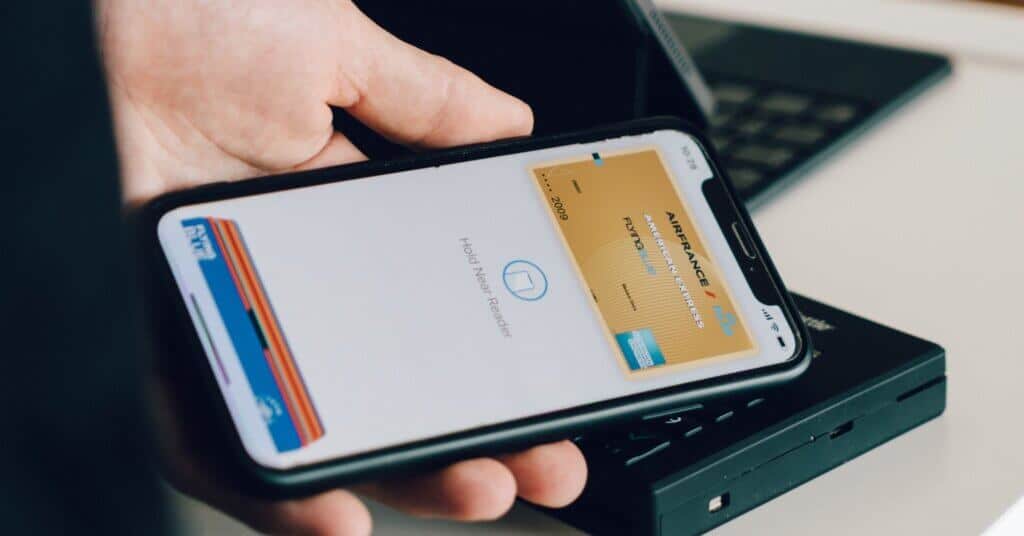

A pass-through e-wallet is a type of digital wallet that does not hold a balance by itself but passes the transaction through to another payment instrument. Some examples of pass-through e-wallets are ApplePay or GooglePay. ApplePay simply passes the transaction to the customer’s credit card or bank account. Customers don’t load money onto ApplePay itself.

Cash-payment methods let customers who don’t have either a credit card or a bank account shop online. At the online checkout, they select the cash-payment option. This generates a way of linking the online purchase to a cash payment, for instance a unique ID number or a printable bar code. The customer takes this to a participating store and pays. The store sends their payment to the online merchant, along with the unique identifier. The merchant then ships the customer’s order.

PPRO offers multiple cash-based payment methods, such as Multibanco, OXXO and Rapipago.

Prepaid vouchers

Customers can usually buy prepaid vouchers at participating stores or online. Each voucher is printed with a code, which the customer inputs at checkout to pay for their online purchase.

How to know which alternative local payment methods to offer

Which payment method varies from country to country. Dutch consumers use the bank-transfer app iDEAL in almost 60% of transactions [1]. But in neighbouring Belgium all bank-transfer apps combined only have a 19% market share [2].

The type of alternative payment method preferred may also differ within markets. In the Philippines, most shoppers use digital payment methods [3]. But 65% of Filipinos don’t have a bank account. For them, cash is king [3].

PPRO is a fintech company that globalises payment platforms for businesses, so they can offer more choice at the checkout and boost cross-border sales. Based on your goals, we can help you work out which alternative payment methods to offer in any market.

Any business that hopes to succeed in any market, whether it’s selling cross-border or opening a local affiliate, must accept local payments. Organisations looking to reach global consumers also need to rethink the label, in many markets what’s called ‘alternative’ is simply how people pay.

Not offering a payment method which consumers know and trust can cause cart abandonment rates of up to 44% [4]. To reduce cart abandonment, merchants must offer the preferred local payment methods for each country

Merchant fees on alternative payment methods vary. But they are usually significantly lower than the fees charged by mainstream payment methods.

Yes, if you integrate them well. There are too many alternative payment methods to generalise about topics such as security, risk or compliance. But PPRO can help you select payment methods for your target market based on both their relevance and things such as security and compliance. We can also help you to add extra layers of security, for instance to prevent chargeback fraud and improve fraud detection.

You can integrate each alternative payment method yourself. This involves setting up a bespoke contract. You’ll then have to integrate, test and validate the payment method yourself. That includes running compliance and legal checks — and so on. Or you can work with a payment specialist, such as PPRO.

At PPRO, we’ve built an infrastructure that lets you launch multiple payment methods at speed and avoid all the contractual and operational complexities along the way. You benefit from a single, straightforward integration. We provide ongoing support and remove the need to worry about legal or contractual details.

These categories often overlap with each other. But they are not exactly the same.

The meaning of ‘alternative payment method’ depends on the context. It can simply mean payment methods other than cards. But many people understand it specifically to mean cryptocurrencies such as Blockchain or Ethereum.

‘Local payment methods’ are any payment methods which are popular or dominant in any given market. In many countries, these are not just alternatives, they are the primary way people pay. For instance, in China, AliPay has a market share of over 50% for online payments [5], making it a locally preferred payment method.

A digital payment method, for instance an e-wallet, can be used both online and instore.

FOOTNOTES

More news

Browse the latest in the world of payments